Tesla: Trinity

two kinds of squeezes, blind index buying and the world's biggest pay package

In my investing activity I usually focus on an individual company’s financial statements, products, management, industry cycle and competitive position. Trying to understand whether the valuation of a company deviates from its value is the core of my activity, this approach makes me “fundamental” investor. To improve my investing practive and broaden my horizon, I want to adapt a more holistic approach.

Thanks to Micheal Green and "Girolamo Pandolfi da Casio" my eyes have been opened to the importance of the sometimes arcane domains of derivatives and market structure. These factors are especially important when trying to understand a phenomenon like the meteoric rise in Tesla’s valuation:

What follows is not about Tesla’s relative position in batteries, insurance or autonomous driving, I’m also not going to spend any time on the financials of the firm itself. To learn more about the fundamentals, consider Christopher Bloomstran’s thread below:

A lot of what I am going to say has already been covered in @INArteCarloDoss‘s brilliant thread, I’ll expand slightly on his important insights:

One: Gamma + Short Squeeze

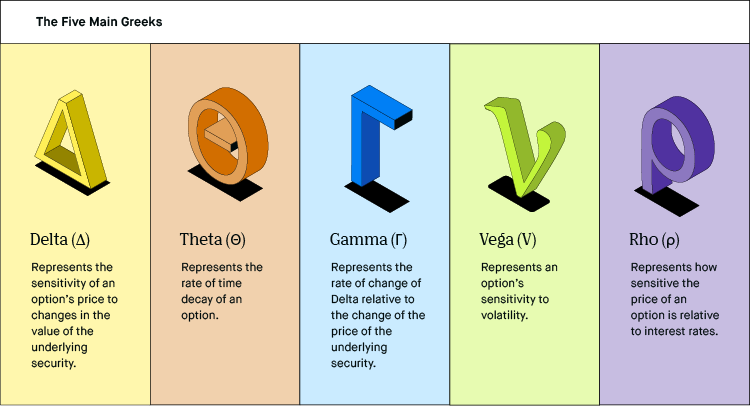

An option is a contract between two parties that allows its buyer to exchange a given amount of stock for a predefined price within a certain period of time. The right to buy is referred to as a “call” and the right to sell is known as a “put”. A call might look like this: “I give you the option to buy 100 shares of company X at a price of $100 a share within the next 6 months”. An option is a derivative, because its value is derived from the value of another financial asset - its underlying. The value of such an option will depend on a number of factors, which are commonly known as the greeks:

The difference of the price of the underlying to the strike, the volatility of the underlying, the remaining time of the option and the interest rate (several additional factors can be added here - a lot of ink has been spilled on the subject), feel free to dig deeper into option pricing.

Using the Black-Scholes options formula, we can use partial derivatives (“what happens to the price of the option if the factor moves by one unit“) to understand the impact of changes in each factor on the value of the option. Without getting too mathematical, let’s try to build an intuition: If you have the right to buy something for $100 and it can be traded for $200 today, then this right is very valuable. If you have the right to sell a given share at $100, but it is trading at $200, then this right is close to worthless. If an underlying stock swings widely (it has a high volatility) then it is more likely to move away from its current price and might fall above or below its strike.

While the point of view of the option buyer is well understood, the behavior of the seller, typically a market maker (MM), is also important to consider. If you sell call options to somebody, you have to carefully hedge your risks in order to not lose money - you are on the hook to deliver a certain amount of stock in the future and there is no theoretical limit to how high those shares may rise. Market makers engage in Delta-hedging, to minimize their exposure to the changes in value of the underlying. When selling a call, any movement of the underlying that gets closer to the strike, means it gets more likely that the option will be exercised. For that reason it is prudent to buy the underlying. This purchasing activity in turn increases the price of the underlying, leading to more buying, leading to more options hedging, leading to more buying … ad infinitum. For an extended take on the infinite gamma-squeeze observation, please consider this reddit post

Tesla has been one of the most widely shorted stocks in the world for a few years now, so the parabolic rise of Tesla triggers a second kind of squeeze: the short squeeze: all those who have borrowed shares and sold them in the hopes of being able to buy them back later at a lower price and thus bag a profit, are forced to cover their short by buying the very stock they shorted. Those who have lent the shares to them have what is called a margin requirement, as a short blows up, the short seller will have to provide more collateral. Closing the short by buying the shares once again contributing to rising prices, more gamma and short squeezing. You know the drill.

Two: blind buying

A stock index is a list of companies that adhere to certain criteria, for example “all companies in the energy sector with revenues above $10bn“. An ETF is a financial instrument that replicates an index, it buys the companies that are on an index. For a market-cap (outstanding shares * price per share) weighted index, the more valuable a stock is, the more if its shares the ETF has to buy.

Tesla pulled out all stops to meet the criteria of the biggest and most well-known stock in index in the world, the S&P500. Once Tesla became part of the index, all the ETFs that replicate the S&P500 (and there are a lot of them) had to buy Tesla shares. These passive funds don’t perform any stock analysis or valuation, they just buy whatever is in the index according to the weighting of the stock. The more valuable Tesla gets, the more shares they will buy. Any movement that happens in the market gets excacerbated through these funds, buying begets buying, selling begets more selling.

The timing of finishing the two squeezes described above into the hands of passive investors who don’t perform equity valuation is truly brilliant - a move for the financial history books. The investors around the world who have put their savings into S&P500 ETFs have paid the highest possible price for Tesla shares.

Three: executive compensation

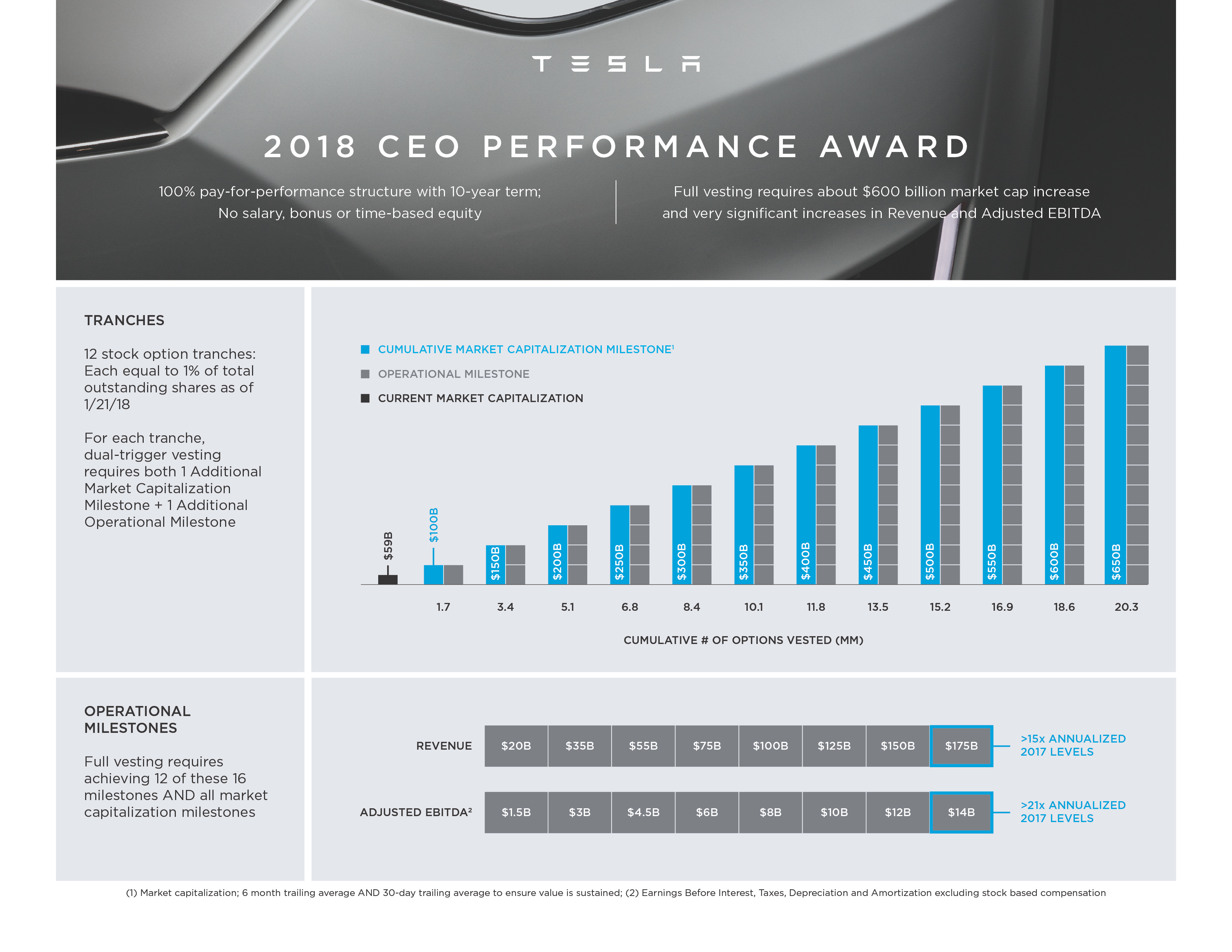

The CEO of Tesla has an extremely aggressive compensation package that is tied to the operational performance of the business and its market capitalization.

There are 12 tranches of stock options that are equal to 1% of the outstanding shares as of January 1st 2018. To get to the next tranche, one market cap goal and one operational goal has to be reached and. I have not been able to figure out whether the goals have to be met simulatenously to trigger the payout or whether it is sufficient that one of the twin-goals has been met at any point in the past, we shall see.

Tesla’s Q4 2017 quarterly report states that “As of February 14, 2018, there were 168,919,941 shares of the registrant’s Common Stock outstanding”. On August 31. 2020 a 5-1 stock split came into effect, so 5 x 168,919,941 is roughly 844,599,705. The strike price on these options is $70.01

Every $50bn increase in the market cap triggers another tranche of options allowing Musk to purchase shares at a deeply discounted price. The 12th and final tranche gets paid out if the market capitalization is above $650bn for a given amount of time. At the time of writing, one share is worth ~$709, as of the latest regulatory filing from July 22 2021, the number of outstanding shares is 990,015,158, yielding a market capitalization of slightly more than $700bn (the share count has likely increased since the date of the filing). A more complete picture is provided by looking at the fully-diluted share count which includes convertible notes and the stock based compensation for other Tesla employees. While the market cap goals have been reached, there is still quite a lot of work to do to meet the operational goals set out in the compensation package. Using the extremly rich valuation of Tesla as a weapon an acquiring another company seems like the easist way to get there.

What’s next?

The forces that propelled Tesla’s share price upwards, also work the other way. If the price stops rising and volatility comes down, the delta-hedges will be decreased and Tesla’s share price goes into reverse with passive funds reinforcing such a movement.

Who is (are) the market maker for $TSLA options? Citadel? They already have lots of shares. Doesn't seem logical that a Market Maker who wants to be hedged wouldn't buy shares within a few microseconds of selling a call and vice-versa. What are the rules for setting bid/ask spreads for market makers? Seems they would be miles apart. When some one party balls thousands of calls soon to expire soon and quite a ways out of the money, is the spread such that they can make a profit by selling their calls back to the market maker (or whoever) if they have gamma squeezed the share price up 1% or so? Or does it cost them money to make the share price go up? It happens often. If they consistently lose then there must be good reason that they keep doing it. We need details, not just definitions of what is a gamma squeeze.